7 points you need to know about the IOSS and customs reform from July 1, 2026

Strategic insights and operational readiness for cross-border E-commerce

Executive Summary

The European Union is introducing comprehensive structural updates to its cross-border e-commerce framework under Council Regulation (EU) 2026/382. Effective July 1, 2026, the traditional €150 customs duty exemption is removed, replaced by a streamlined flat-rate tariff system and enhanced product data tracking. This article provides a professional analysis of the seven critical aspects businesses must understand to adjust their international supply chains, compliance workflows, and software configurations.

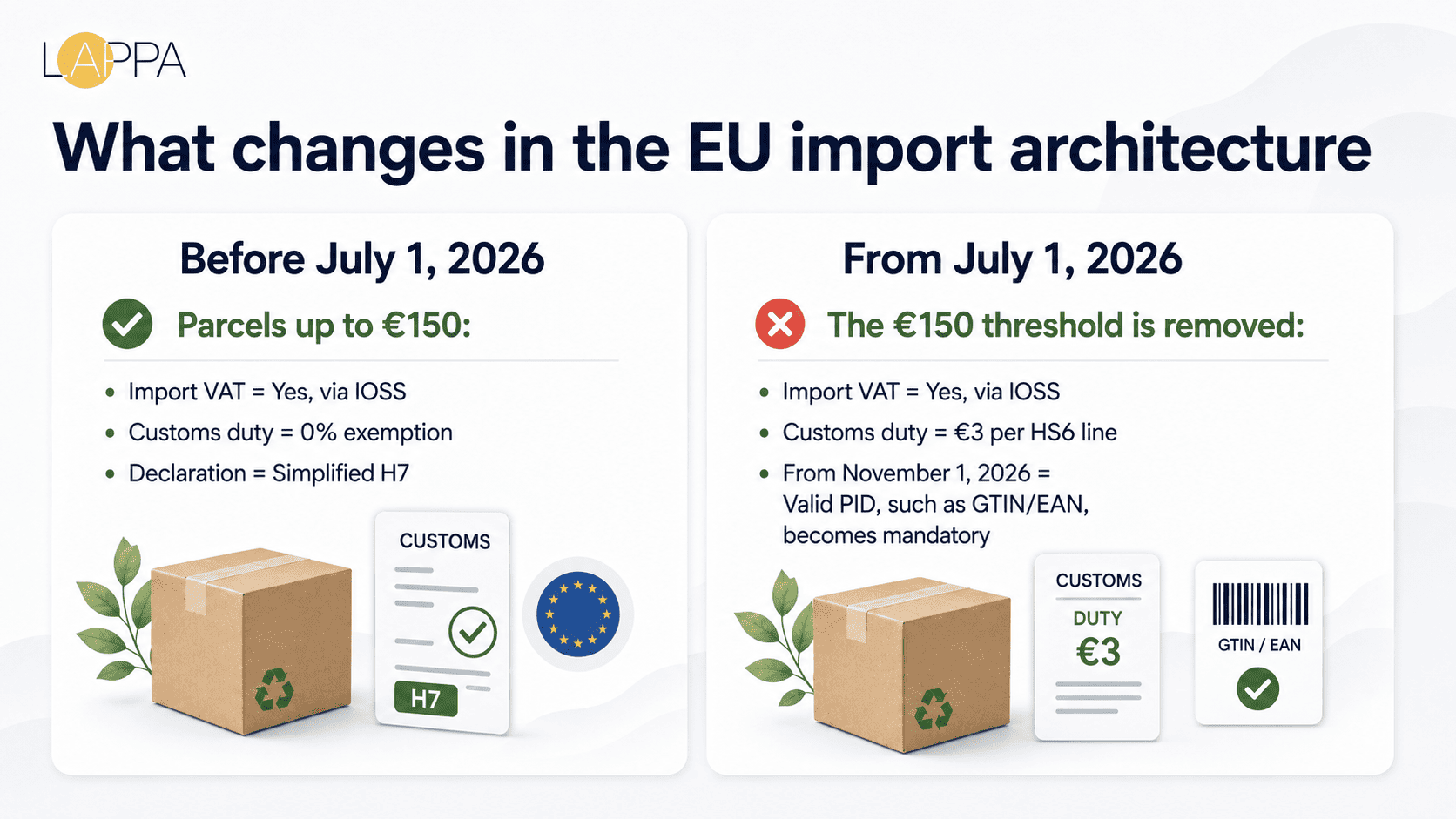

1. Complete removal of the €150 threshold

Starting July 1, 2026, the long-standing €150 de minimis threshold for customs duty exemptions on B2C imports will no longer exist within the European Union. While the 2021 e-commerce reform successfully applied import VAT to all low-value goods, customs duties remained exempt for parcels under €150. Under the updated regulations, every commercial package entering the EU from a third country will be subject to standard customs processing and duty obligations, completely eliminating the distinction based on low transaction values.

2. Introduction of the €3 flat-rate duty

To prevent operational delays and minimize processing complexities across European customs checkpoints, a simplified flat-rate duty is being implemented. From July 1, 2026, until June 30, 2028, a flat fee of €3 will apply to low-value consumer shipments. This transitional measure provides international merchants and postal networks with a straightforward, predictable cost structure before the EU transitions fully to the highly automated EU Customs Data Hub system planned for 2028.

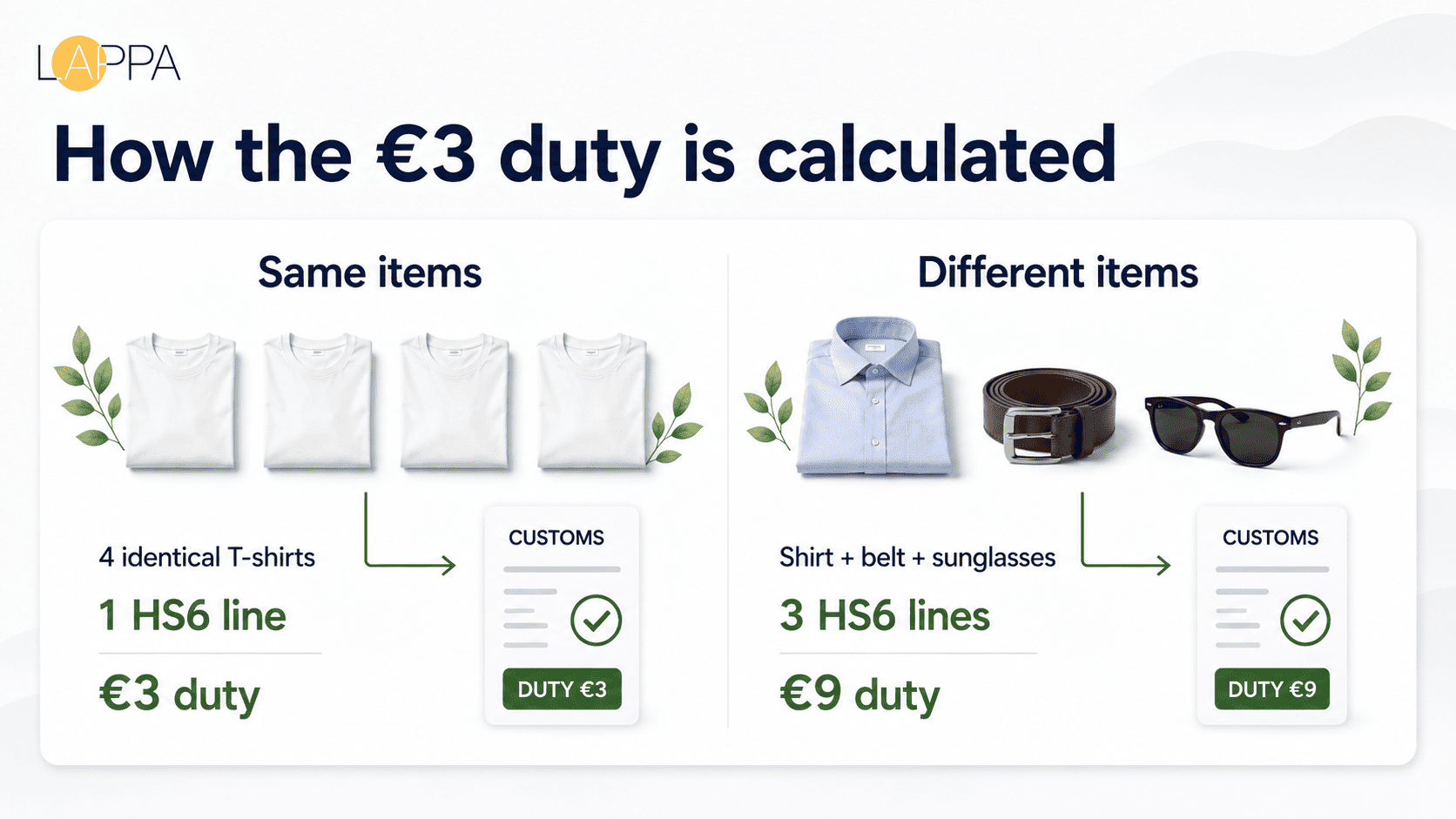

3. The per-item (HS6 line) calculation mechanism

An essential technical characteristic of the €3 flat rate is that it is assessed per unique item line within the electronic customs declaration, rather than per physical box or overall order. Item lines are classified based on the 6-digit Harmonized System (HS6) tariff code.

- Single HS6 Line: A package containing multiple identical items (e.g., four cotton shirts) shares the same HS6 code, generating one line in the declaration. The total flat duty remains €3.

- Multiple HS6 Lines: A package containing different types of goods (e.g., a shirt, a leather belt, and a pair of sunglasses) requires three distinct HS6 classifications. This creates three separate lines in the declaration, resulting in a total duty of €9 (€3 × 3), even if the combined monetary value is low.

4. Why IOSS handles VAT, not customs duties

A key operational distinction must be maintained between import taxes and customs duties. The Import One-Stop Shop (IOSS) registration framework—whether maintained via Latvia, France, or other regional tax portals—remains strictly a mechanism for collecting, reporting, and remitting import VAT at checkout. IOSS cannot be utilized to declare or clear customs duties. Because the €3 flat rate is a distinct customs duty, it is administered directly at the physical EU border by customs authorities, meaning the VAT and customs tracks operate in parallel.

5. Navigating the transition from DAP to DDP models

To ensure an optimal and seamless delivery experience for consumers, international businesses are encouraged to transition from Delivered Duty Unpaid (DAP/DDU) to Delivered Duty Paid (DDP) shipping terms. Under a DAP approach, the regional postal or courier service must collect the €3 duty, along with standard carrier administrative handling fees, directly from the consumer prior to final delivery. Shifting to a DDP model allows e-commerce platforms to calculate the duty dynamically during online checkout, integrate it into the initial transaction, and settle it transparently via their logistics provider’s billing account.

6. Mandatory product identifiers (PID) by November 2026

While the flat-rate duty begins in July, a secondary data compliance milestone occurs on November 1, 2026. From this date, providing valid Product Identifiers (PIDs) within the electronic H7 customs dataset becomes mandatory. Acceptable PIDs include Global Trade Item Numbers (GTIN), EAN, or UPC barcodes. These identifiers allow automated customs verification systems to validate that the electronic declaration matches global product databases, facilitating expedited green-channel clearance for compliant shipments.

7. Operational readiness checklist for E-commerce platforms

Achieving full compliance with the 2026 requirements involves straightforward technical updates. Merchants should focus on updating catalog structures to ensure all SKUs carry correct 6-digit HS codes, adjusting checkout software to aggregate and multiply the €3 fee based on unique HS6 lines, and coordinating with logistics networks to guarantee automated DDP data transmission. Proactive alignment ensures that international delivery networks continue to operate efficiently without delays at the border.

Key compliance milestones timeline

| Milestone date | Core regulatory change | Strategic business impact |

| July 1, 2026 | Abolition of €150 limit. Implementation of €3 flat duty per HS6 line. | Pricing updates required at checkout to avoid margin reduction. |

| November 1, 2026 | Mandatory submission of Product Identifiers (GTIN/EAN) in H7 dataset. | Requires inventory data synchronization with courier electronic logs. |

| July 1, 2028 | Transition to EU Customs Data Hub and multi-tier category tariffs. | Long-term transition to structured percentage-based category buckets. |

Ready to update your checkout for the €3 flat duty? Get a free quote or book a demo to configure your IOSS and customs compliance with an expert.

FAQ

EU Customs Reform 2026

Does the €3 flat duty apply to every parcel entering the EU from July 1, 2026

The €3 flat duty applies to all B2C consignments with an intrinsic value up to €150 imported from non-EU countries under Council Regulation (EU) 2026/382. B2B shipments going to VAT-registered recipients follow standard customs duty rates instead. Goods covered by preferential trade agreements may retain reduced rates — but only if VAT was not collected via IOSS and the declaration uses the standard H1 form, not H7.

How is the €3 duty calculated when a parcel contains multiple products

The duty is charged per HS6 tariff line, not per parcel. A package with one product type generates one €3 charge regardless of quantity. A package mixing three product categories — say, a shirt, a belt, and sunglasses — generates three separate HS6 lines and a €9 total duty. Accurate HS code classification at SKU level is not optional from July 1, 2026: it directly determines the customs cost passed to the consumer or absorbed by the merchant.

Does IOSS registration cover the new €3 customs duty

No. IOSS handles import VAT collection, reporting, and remittance at checkout. The €3 flat rate is a customs duty administered at the EU border by customs authorities — a separate track entirely. Sellers registered for IOSS still benefit from faster customs clearance and avoid VAT being charged on top of the €3 duty itself, but IOSS does not declare or clear customs duties.

What are Product Identifiers and why do they become mandatory in November 2026

Product Identifiers — GTIN, EAN, or UPC barcodes — must be included in the H7 electronic customs dataset from November 1, 2026. Customs authorities use PIDs to match declarations against global product databases automatically, enabling green-channel clearance for compliant shipments. Sellers without valid PIDs assigned to every SKU face manual customs checks and potential delays from that date. PIDs can be submitted voluntarily from July 1, 2026 to test systems ahead of the hard deadline.

Should cross-border sellers switch from DAP to DDP shipping after July 2026

Yes. Under DAP terms, the carrier collects the €3 duty plus its own administrative handling fee directly from the consumer before delivery — a friction point that increases failed deliveries and damages customer experience. Switching to DDP moves duty calculation to checkout, gives the consumer a guaranteed final price, and settles the duty through the logistics provider’s billing account. For high-volume sellers, DDP also simplifies reconciliation and reduces carrier surcharges per shipment.