EU Countries Requiring EPR Textile Registration in 2026: A Seller’s Guide

Under the updated Waste Framework Directive, all 27 EU member states are required to establish mandatory EPR schemes for textiles by April 2028. However, several countries have jumped ahead, making registration a legal requirement well before the deadline.

Who must register for EPR Textile in EU

The obligation generally applies to any company that first places textile products on the market of a specific country. This includes:

- Domestic manufacturers based in the EU country.

- Importers bringing goods from outside the EU (e.g., from China or the USA).

- Cross-border e-commerce sellers shipping directly to consumers in that country.

Mandatory registration countries in 2026

By 2026, sellers must be registered and paying eco-contributions in the following four countries. Most notably, there is no “de-minimis” threshold—the obligation starts from the very first item sold.

| Country | Effective Date | Threshold for Registration | Covered Categories |

| France | Since 2007 | From the 1st unit. Simplified fee for <5,000 units. | Clothing, footwear, and household linens. |

| Netherlands | July 2023 | From the 1st unit. No weight/volume exemptions. | Consumer and work clothing, bed, table, and kitchen linens. |

| Hungary | July 2023 | From the 1st unit. Reporting is quarterly. | Clothing, accessories, footwear, carpets, and household textiles. |

| Latvia | July 2024 | From the 1st unit. Natural resources tax applies. | Clothing, footwear, blankets, curtains, and linens. |

Countries entering implementation Phase

While the four countries above have active enforcement, several others are expected to have their national systems fully operational or in a “grace period” by 2026:

- Spain: Currently finalising Royal Decrees. Full EPR obligations for textiles are expected to be enforced by 2025/2026.

- Italy: The legislative framework is ready, and specialized Producer Responsibility Organizations (PROs) are already forming to manage the upcoming mandatory system.

- Sweden & Denmark: These countries already have advanced collection systems and are currently aligning their national laws with the 2028 EU deadline.

Compliance checklist for 2026

If you are selling textiles in Europe, you should take the following steps to avoid heavy fines (which can reach tens of thousands of Euros in France or Spain):

- Identify your role: Determine if you are the “producer” (first placer) in each market.

- Join a PRO: Register with a Producer Responsibility Organization (e.g., Refashion in France or Stichting UPV in the Netherlands).

- Appoint an Authorized Representative: If your company is not legally established in the country of sale (especially critical for Hungary and Spain), you may need a local representative.

- Track Data: Start tracking the weight and material composition of every textile item sold per country.

- Report and pay

What is EPR for Textile

Extended Producer Responsibility is a policy approach that shifts the financial and operational responsibility for end-of-life product management from municipalities and taxpayers to the companies that introduce products into the marketplace. It’s a fundamental shift in how the textile industry accounts for the full life cost of clothing and household fabrics. This is precisely what EPR textiles regulation was designed to address.

Under EPR, a producer can’t just sell a garment and walk away. Instead, they are financially responsible for seeing that garment collected, sorted, then recycled or reused after the consumer throws it away. In practice, this means that eco-contributions – fees calculated on the weight or volume of textiles placed on the market – are paid into a collective fund managed by a Producer Responsibility Organization (PRO). The money in that fund is then used to pay for collection infrastructure, sorting facilities and recycling programmes across the country.

EPR for textiles may be an alien compliance burden for smaller sellers and cross-border e-commerce operators. But it is best viewed as a cost of market access and spreading swiftly to the rest of the bloc. For any seller in the EU, EPR textiles compliance is no longer optional.

What is considered as EPR Textiles

Many businesses underestimate the breadth of the definition of a “textile” under EPR schemes. It’s not just clothes. The following product categories are generally covered in the various national systems already in operation:

All types of clothing and apparel, including outerwear, underclothing, sportswear and workwear. Any footwear, e.g. shoes, boots and sandals, of any material. Household linen such as bed sheets, pillowcases, duvet covers, towels, tablecloths and kitchen textiles. Soft furnishings such as curtains, blinds, upholstery fabrics and decorative cushion covers. Carpets and rugs. Textile materials for making hats, scarves, gloves and bags, and other accessories. Certain technical and industrial textiles in certain jurisdictions.

The exact list varies by country, understanding the scope of EPR textile obligations per market is essential before entering any new EU country. For example, Hungary explicitly includes carpets and accessories in its EPR scope, whereas France has traditionally focused on clothing, footwear and household linen. Instead of assuming that the product definition is the same across the EU, sellers should check the national legislation implementing the directive when entering a new market.

Fashion as i main target of EPR Textile

The European Commission’s EU Strategy for Sustainable and Circular Textiles, published in 2022, provides the policy foundation for rolling out EPR across the bloc. Known as the EU textile strategy, this policy framework forms the backbone of EPR rollout across member states.It was a conscious effort to counter the excesses of the fast-fashion model.

That’s a serious problem. On average, Europeans consume 26 kg of textile products per person per year and discard about 11 kg. The fashion industry is responsible for around 10% of the world’s annual carbon dioxide emissions – more than international aviation and maritime shipping combined. The EU is in the fourth highest pressure category for the environment and climate, behind food, housing and transport.

These impacts are compounded by fast fashion, which shortens product lifecycles. If clothes are made to be worn only a handful of times before being thrown away, the waste becomes huge, and the financial incentive to collect and recycle it is low. The EPR is the EU’s key tool to address this market failure . By charging producers for the end-of-life management according to the volume they place on the market, a direct financial incentive to design products that last longer and are more recyclable is created.

Eco-modulation – the application of fees based on durability, recyclability or use of recycled content – is the main mechanism by which EPR schemes incentivise producers to move away from the principles of fast fashion.The EU textile strategy continues to drive these design incentives forward. The EU textile strategy continues to drive these design incentives forward

Europe coverage of Textiles EPR

Not all textiles on the market will fall under EPR obligations. Coverage of textiles Europe-wide is extensive but not universal The coverage is extensive, but most national schemes expressly exclude certain categories. Typical exclusions are:

- Medical textiles and regulated products for medical devices.

- Industrial or professional textiles never reaching consumers.

- Products sold second hand, where the original producer has already fulfilled his obligation.

- Very small business operators in some jurisdictions (but this exception is being phased out across the EU).

It’s important to understand that EPR applies to the product itself, not the transaction. Understanding how textile obligations apply across Europe starts with identifying where the product is placed on the market. Where a seller fulfils orders from a warehouse located in France for consumption by French consumers, the seller is subject to French EPR obligations, regardless of where their company is incorporated. The trigger is putting the product on that national market – not the legal seat of business.

This brings about a situation for e-commerce sellers where EPR registrations may be required simultaneously in different countries. A seller shipping to consumers in France, The Netherlands, Hungary and Latvia must be registered in all four, with separate eco-contribution accounts and reporting cycles for each. The textiles Europe compliance map is therefore not one registration but many.

Producer for the Textile Sector

The definition of “producer” is the central question in EPR compliance, and it is answered differently depending on the supply chain position of the business in question.No other definition matters more to businesses operating in the textile sector

- A domestic manufacturer that produces textiles within an EU member state and sells them under its own brand is unambiguously the producer and bears full EPR responsibility in its home market. Within the broader textiles sector, domestic manufacturers bear the most straightforward compliance obligations.

- An importer that brings textile products from outside the EU — whether from Asia, the United States, or elsewhere — and places them on an EU national market is treated as the producer for EPR purposes. The overseas manufacturer has no legal standing within the EU regulatory framework and cannot be held responsible.

- A brand owner or licensee that commissions the manufacture of textiles under its brand name, even if production is outsourced, is generally considered the producer because it is the entity making the commercial decision to place the product on the market.

- A marketplace or platform seller that sells its own goods through third-party platforms remains the producer for those goods. However, when a marketplace facilitates sales by third-party sellers to EU consumers, the responsibility typically remains with the individual seller — unless the marketplace has explicitly assumed EPR obligations on their behalf, as some platforms have begun to do.

- A cross-border e-commerce seller based outside the EU that ships directly to EU consumers is treated as the producer in each country of delivery. This is the scenario that catches the largest number of non-EU businesses off guard. There is no de minimis threshold based on the legal establishment of the seller — the obligation flows from the act of sale into that market.

Registration and Rollout for a future years

- By April 2028, all 27 EU member states must have in place operational EPR schemes for textiles, according to the revised Waste Framework Directive. This deadline was formalised through publication in the Official EU Journal and is binding on all member states. However, the real time of implementation is much more condensed for sellers.

- 2023-2024 (Already in force) Active enforcement: France (since 2007), Netherlands (July 2023), Hungary (July 2023), Latvia (July 2024) “Unregistered sellers in these markets already face the risk of enforcement action.

- 2025–2026: Spain is nearing the end of its implementation of Royal Decrees, with enforcement for textiles expected to begin during this period. Italy’s PRO ecosystem is coming together quickly with legislation largely in place. Sellers should be actively preparing now for compliance in these two major markets.

- 2026-2027: Germany, Belgium, Poland and Austria are expected to transpose the directive and launch national EPR schemes. In particular, Germany is expected to have a rigorous and actively enforced system due to the size of its consumer market and its established track record in packaging EPR enforcement.

- 2027-2028: The remaining EU member states (including Central and Eastern Europe) are expected to complete their national implementations in the run up to the April 2028 deadline.Sellers should monitor the Official EU Journal for implementing regulations specific to each country.

- Post-2028: Intensification of enforcement and refinement of eco-modulation are expected. Each update to Digital Product Passport requirements will likewise be published in the official journal of the EU. A requirement for a Digital Product Passport, which will require textile products to carry sustainability data that machines can read, is being phased in from around 2030.All of these developments stem from the broader EU textiles strategy objectives set in 2022.

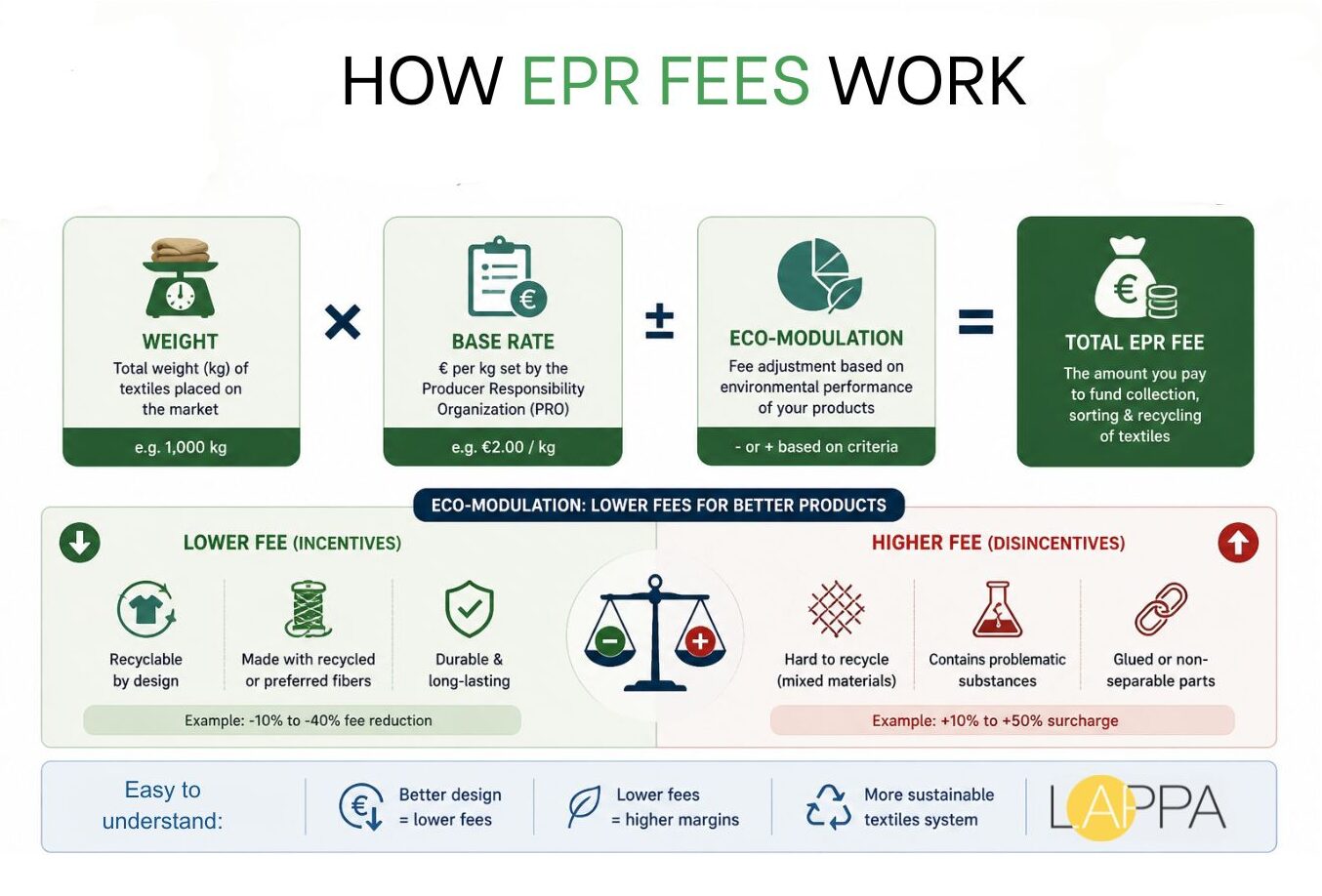

Eco-Fees and Eco-Modulation for Textiles Europe

EPR schemes are financially driven by eco-contributions . This financial architecture is central to the EU textile regulatory model The PRO fund charges producers a fee for each country in which they are registered . This is usually based on the number of kilograms of textiles that are put on the market . These are set by each PRO and vary widely between countries and product categories.

Refashion’s model in France is based on a tiered fee system, with heavier, bulkier items like curtains and carpets attracting different charges than lightweight clothing. Small producers that sell less than 5,000 units per year benefit from an easier administrative process and a reduced flat fee instead of a weight-based fee.Each country applies its own version of EU textiles eco-modulation criteria.

Eco-modulation means increasing or decreasing the level of standard fees depending on how well the product performs for the environment. A garment produced from recycled fibers, designed for disassembly and clearly labeled with care instructions could be charged a lower eco-contribution than a comparable garment made from virgin synthetic fibers with no recyclability. On the other hand, there are surcharges for products with problematic substances, inseparable mixed materials or glued components which cannot be recycled.

In practice this means that product design decisions made years before a garment hits the shops can have a direct impact on sellers in terms of ongoing compliance costs. As eco-modulation gets more sophisticated, firms investing money in design for recyclability today are building a structural cost advantage.As the EU textile framework matures, these cost differentials will only grow

How to report Reporting for Sustainable Textiles

Compliance with EPR rules goes beyond just registration and fee payment. It also calls for systematic collection of data and regular reporting on the quantities, weights and composition of textiles placed on each national market. Systematic reporting is what transforms a business into a producer of genuinely sustainable textiles

Today the reporting obligations differ from country to country. Hungary needs quarterly reporting. France and the Netherlands are on annual cycles with some interim data submissions. As schemes mature, reporting granularity is expected to increase, moving towards material-level composition data (e.g. percentage cotton, polyester, elastane etc) rather than simple weight by category figures.

The Digital Product Passport (DPP) is coming in under the Ecodesign for Sustainable Products Regulation and will be linked with EPR reporting in due course. The DPP will add a unique, machine-readable identifier to each textile product that will provide information on its materials, origin, repairability and end-of-life instructions. For EPR purposes, the DPP will provide regulators with a standardised, verifiable data source to cross-check against reported volumes.The DPP reflects the EU’s wider goal of making sustainability in textiles verifiable at every stage of the supply chain.

Companies with strong internal data systems in place today – tracking things like material composition at the SKU level, unit weights and sales volumes market by market – will be in a much better position to meet current EPR reporting and future DPP requirements than those who attempt to reconstruct this data in retrospect.This data discipline is the foundation of a credible sustainable textiles strategy.

Penalties for non-compliance in Europe

The severity of penalties for non-compliance varies widely between Member States, but the trend is towards more active enforcement and higher financial consequences. Enforcement of obligations on textile in Europe is accelerating as national authorities build experience

In France, which has had the system since 2007, the authorities have decades of enforcement experience. If you fail to register or you under-report, you could be fined tens of thousands of euros. If you repeatedly break the rules, you could even be barred from the market. Imported textile shipments may be selected by customs authorities for compliance checks at the border.

The Netherlands and Hungary have both signalled an intention to actively enforce their 2023 schemes, with market surveillance authorities empowered to investigate and sanction non-compliant producers. In Latvia, if you do not pay the natural resources tax that funds the system, you will be subject to certain financial penalties.

Spain’s new textile scheme is likely to have teeth similar to the country’s packaging EPR system, which already levies fines of up to €100,000 for serious breaches.

In addition to direct financial penalties, the reputational risk of non-compliance is becoming increasingly material. Companies selling textiles in European markets must account for both financial and reputational exposure. With sustainability due diligence reporting obligations increasing across the EU (including under the Corporate Sustainability Reporting Directive), non-compliance with EPR obligations could be flagged as a governance failure in regulatory filings, supplier audits and investor disclosures.This reflects the broader trajectory — textile in Europe is entering a period of rigorous regulatory scrutiny.

Tax calculations for Textiles Europe

For many businesses, the first thing that comes to mind when it comes to EPR compliance is the eco-contribution fee itself. But the full financial story is more complex.

Eco-contributions are an operating cost and must be included in product pricing models. For companies operating on razor-thin margins – which is common in highly competitive fast fashion segments – not factoring in these costs upfront can eat into profitability.

In addition to the eco-contribution, PRO membership itself has administrative fees. Some PROs charge a fixed fee for the membership per year, others a percentage of the declared volume. Sellers operating in multiple markets will experience duplicate costs in each jurisdiction.

In many countries, non-EU sellers are legally required to appoint an Authorised Representative – which adds another layer of cost. Typical service fees run from a few hundred to several thousand Euros per annum per country, depending on the volume of activity and the scope of services provided.

eco-contributions are not subject to VAT in all jurisdictions on the tax side but the interaction between EPR fees and the VAT treatment of the underlying sales should be reviewed with a specialist, especially for cross-border e-commerce sellers already navigating the EU’s One Stop Shop VAT regime.

Recommendation of what is better to avoid

There are several common patterns to the most frequent compliance failures seen across EPR programmes.

Assuming that there is a de minimis threshold when there is none. In some countries EPR is packaged, while in France, the Netherlands, Hungary and Latvia, textile EPR is applied from the first unit sold. If a seller defers registration on the assumption that volume thresholds must first be met, it may be subject to significant retroactive liability.

Registered in the country of incorporation of the company, not the country of sale. EPR obligations are triggered by placing on the market, not legal establishment. If a business in Germany sells to Dutch consumers, it has to register in the Netherlands

.

E-commerce is treated differently from retail. EU tax and customs authorities are getting better and better at spotting cross-border e-commerce sellers, using VAT registration data, marketplace operator disclosures and customs declarations. The assumption that digital sales are less visible to regulators is becoming a more dangerous assumption.

Underreporting due to incomplete internal information. Sellers without the ability to reconcile unit sales to weight data by country may risk filing inaccurate declarations. In a DPP future, differences between declared volumes and product passport data will be identifiable.

Combining packaging EPR and clothing EPR. Many companies already signed up to packaging EPR schemes think they have done their bit. Textile EPR is a distinct parallel system with its own PROs, registration and fee structures.

What businesses may face

The EPR transition offers real compliance complexity – but it also offers structural opportunities for businesses willing to engage with it strategically.

On the challenge side, the fragmentation of national EPR systems across 27 member states means that there is no single registration, no single PRO and no single fee structure that covers the entire EU. A business selling into ten EU markets might need ten separate registrations, ten sets of reporting obligations and ten ongoing relationships with local PROs or authorised representatives. This requires significant internal compliance resource or specialist multi-country EPR service providers to manage at scale.

On the opportunity side, as eco-modulation matures, companies designing truly recyclable products and able to prove so at the material level will benefit from lower eco-contribution rates. They are not just ticking a compliance box, but rather creating a cost structure that becomes more attractive as fee differentials increase. Early adopters of sustainable textile design

EPR compliance data, especially weight-by-material and country-of-sale reporting, also offers business intelligence that can inform decisions on procurement, inventory and product development. Companies that view EPR data as an asset, rather than a burden, will be better positioned to respond to changing consumer preferences for transparency and sustainability credentials.

Practical Steps for compliance

- Companies that take a proactive approach to EPR compliance can control costs, and avoid the penalties and reputational risks of non-compliance.

- Start with a compliance audit. List all of the EU markets you currently or intend to sell textiles to. For each market, identify if an EPR scheme is in place, is coming, or is pending. Specify your producer role for each market.

- Create data infrastructure. Your ERP or order management system must be able to report the total weight of units sold by country by reporting period for each SKU. Now, capture material composition at the SKU level, where possible – this will be required for DPP compliance and increasingly valuable for eco-modulation purposes.

- Sign up with the proper PRO in each active market. In France it’s Refashion. Stichting UPV, The Netherlands. In Hungary the registration is undertaken by the national environmental authority. In Latvia declarations are submitted within natural resources tax.

- If needed appoint authorised representatives. This step should be a priority for non-EU businesses selling into Hungary and Spain in particular, as trading without a local representative in these markets exposes the business to direct enforcement action with no notice period.

- Set aside funds for ongoing compliance costs. Incorporate the cost of PRO memberships, eco-contributions, representative fees and internal reporting resource in the annual cost planning. Model the effect of fees on product pricing, especially in high volume, low margin categories.

- Keep an eye on the legislative pipeline. The textile EPR landscape will continue to evolve materially through 2028 and beyond. Assign a member of your organisation to monitor new national implementations, changes to fee structures and the development of DPP requirements.