Form 1120 vs. Form 1120-F: Who files What, When, and Why it matters

The Internal Revenue Service (IRS) mandates all businesses, whether they are based in the US or not, to record any income they make inside the US. If you don’t file the appropriate form on time, you could face big fines, interest, and even legal problems that get in the way of your business.

Form 1120 (the typical US corporate income tax return) and Form 1120-F (the same thing for foreign organizations with US-sourced income) are the two forms that are most important for US companies to fill out. It’s important to know which rules apply to your firm, what information you need to submit, and when the filing is due, whether you are a US-based corporation or an overseas business that does business in the US.

This book explains everything in simple terms, with real-life examples and straightforward answers to the topics we get asked the most by clients.

What Is From 1120

The main annual tax return that domestic C corporations file with the IRS is Form 1120, sometimes known as the US Corporation Income Tax Return. IIt figures out how much federal income tax a business owes for the year and lists its income, gains, losses, credits, and deductions.

Who Needs to Submit Form 1120

Form 1120 must typically be filed by the following entities:

Domestic C corporations that were established in the US in accordance with federal or state legislation.

Foreign businesses that have chosen to be taxed like domestic businesses.

Some limited liability corporations (LLCs) have chosen to be taxed as corporations (via Form 8832).

Any corporation with no taxable income — a zero-income return is still required in most cases.

IMPORTANT

S corporations file Form 1120-S, not Form 1120. Partnerships use Form 1065. Form 1120 is specifically for C corporations. Choosing the wrong form is one of the most common early mistakes.

What’s reported on Form 1120

The form covers total gross income, cost of goods sold, deductions (salaries, depreciation, interest expense, advertising, etc.), taxable income, and the resulting tax liability. Corporations may also attach supplemental schedules for items such as dividends received, balance sheets (Schedule L), and reconciliation of income (Schedule M-1 or M-3).

What Is IRS Form 1120-F

Form 1120-F is the tax return that international companies that make money from US sources or do business in the US have to file. It is separate from Form 1120 because the US tax obligations of a foreign corporation are more nuanced: they depend on whether the corporation is “engaged in a US trade or business” (ECI rules) and whether applicable tax treaties modify those obligations.

Who Must File Form 1120-F

If a foreign company does any of the following, it must file Form 1120-F:

- Were you in the US for any part of the tax year for business or commerce, even if no money was made?

- Had income, gains, or losses that were classified as effectively related to a US trade or enterprise (ECI).

- Had income from the US that was subject to withholding tax, such as dividends, rent, or royalties that were fixed, determinable, annual, or periodic.

- Wants to claim a refund of US taxes withheld at source.

- The company has a protective return filing obligation; even if it believes it has no US taxable income, filing preserves its right to deductions.

Real-Word Examples

A German GmbH licenses software to a US client for $200,000 per year. The US client withholds 30% tax on these royalty payments and remits it to the IRS. The German GmbH should file Form 1120-F to report this income, claim deductions related to it, and potentially recover over-withheld taxes under the US-Germany tax treaty.

If the GmbH also has a branch office in New York that sells products directly to US customers, the branch income is ECI and must also be reported on Form 1120-F — with a separate branch profits tax calculation.

The Protective Return Filing

One often-overlooked requirement: even a foreign corporation that believes it has no US taxable income should consider filing a timely “protective” Form 1120-F. If it doesn’t file, the IRS is entitled to reject any credits or deductions if it later finds that the business did earn US business revenue, thereby taxing gross income without any offsets. These rights are protected at no extra cost by filing a protective return.

Important Differences: Form 1120 vs. Form 1120-F

While both forms serve as annual corporate tax returns, they differ significantly in scope, complexity, and the rules they apply. The table below summarizes the most important distinctions.

| Criteria | Form 1120 | Form 1120-F |

| Who files | Domestic C corporations (US-incorporated) | Foreign corporations with US income or US business activity |

| Tax base | Worldwide income (with foreign tax credits for taxes paid abroad) | Only US-source income and effectively connected income (ECI) |

| Branch profits tax | Not applicable | Applies — 30% (or reduced treaty rate) on branch profits equivalent to dividend |

| Treaty provisions | Rarely relevant | May reduce or eliminate tax obligations; must be claimed on the return |

| Currency | USD only | USD required; functional currency conversion rules may apply |

| Complexity level | Moderate — straightforward for standard operations | High — requires analysis of ECI vs. FDAP, treaty positions, withholding reconciliation |

| Protective filing | Not applicable | Strongly recommended even when no US taxable income exists |

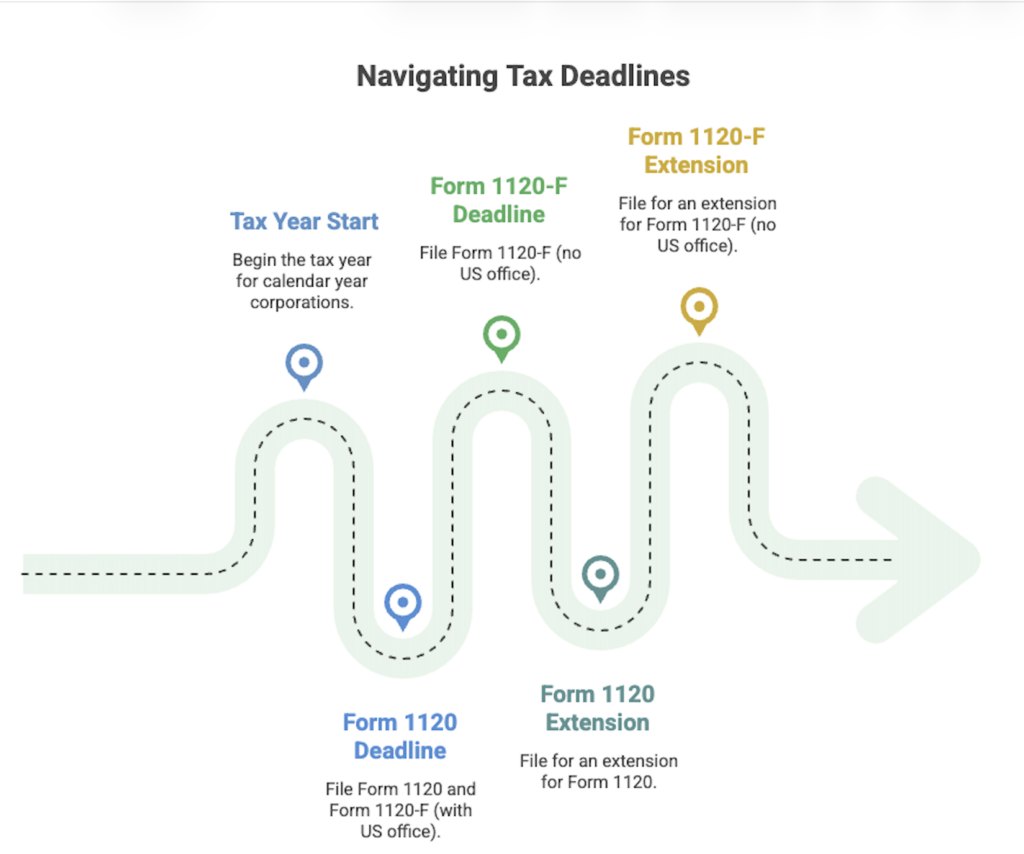

| Standard deadline | April 15 (calendar year filers) | June 15 (if no office or place of business in the US); April 15 otherwise |

Extensions

- Both types let you file late, but it’s crucial to realize that getting more time to file is not the same as getting more time to pay your taxes.

- Form 1120: If you file Form 7004 on time, you will automatically get six more months. People who file for the calendar year have until October 15.

- Form 1120-F also uses Form 7004. Companies from other countries who have to file by June 15 can now do so by December 15.

- You still have to pay any anticipated taxes payable by the original due date to avoid paying interest and late fines.

DON’T CONFUSE FILING WITH PAYMENT

Many businesses request an extension and assume all obligations are deferred. The IRS will charge interest on any unpaid taxes from the initial due date, even if you filed for an extension. Always guess how much you owe and pay it by the original due date.

Filing Deadlines and Extensions

Standard Deadlines

| FORM 1120 — CALENDAR YEAR | FORM 1120 — FISCAL YEAR |

|

April 15 Deadline for C corporations with a calendar tax year ending December 31. |

15th day, 4th month After the close of the fiscal tax year. E.g., fiscal year ending June 30 → October 15. |

| FORM 1120-F — US OFFICE | FORM 1120-F — NO US OFFICE |

|

April 15 Foreign companies that have an office or company in the US have the same deadline as US companies. |

June 15 Foreign corporations with no US office or permanent establishment have an extended automatic deadline. |

Fines for Not Filing or Filing Late

The IRS does not take non-compliance lightly. If you file your taxes late or don’t pay them on time, you will face the following penalties:

Form 1120: If you don’t file, you’ll have to pay 5% of the unpaid tax each month (or part of a month), up to a maximum of 25% of the total unpaid tax.If your return is more than 60 days late, the minimum fine is $450 (2024 figure, adjusted for inflation).

Failure-to-Pay Penalty

If you don’t pay your taxes, you will owe 0.5% of the amount each month, up to 25%. This adds to the consequences for not filing.

Late Filing of Form 1120-F: Special Penalty

If a foreign company doesn’t file its 1120-F on time and the IRS later finds that it had ECI, the IRS may deny all deductions and credits and tax the company’s gross income at the standard 21% corporate rate with no offsets. This punishment can be much worse than a failure-to-file penalty and is often permanent.

Interest on Not Paying Enough

Interest starts to build up on any unpaid taxes every day after the due date. The IRS interest rate is the federal short-term rate plus 3 percentage points, and it changes every three months.

Common Filing Mistakes to Avoid

- Filing the wrong form entirely. Foreign corporations sometimes file Form 1120 when 1120-F is required, or vice versa. This invalidates the filing and can trigger IRS inquiry. Always confirm your entity’s tax residency status before filing.

- Missing the protective filing for foreign corporations. Foreign entities doing any business in the US — even passively — should file a protective Form 1120-F. Not doing so can permanently eliminate your right to deductions if the IRS later asserts US tax liability.

- Failing to report all US-source income on 1120-F. Some foreign corporations report ECI but omit FDAP income (or the reverse). Both categories must be addressed on the return with appropriate withholding reconciliation.

- Not claiming treaty benefits. Many foreign corporations are entitled to reduced withholding rates or exemptions under US tax treaties but fail to claim them—often because the treaty position must be disclosed on the return itself (including Form W-8BEN-E and Treaty Position Disclosure on 1120-F).

- Incorrect or missing Schedule M-3 or L. Larger corporations are required to file Schedule M-3 (reconciliation of financial income to taxable income) and Schedule L (balance sheet). Missing these triggers IRS automated notices and potential penalties.

- Assuming no income means no filing requirement. As noted above, zero income does not automatically eliminate the filing obligation — for either form. A nil return is still required in most circumstances.

Get registered today or book a free consultation with our EPR specialists.

FAQ for 1120-F

Do I need to file Form 1120 if my corporation had no income this year?

- In most cases, yes. The IRS requires domestic C corporations to file Form 1120 for every tax year the corporation is in existence, regardless of whether it generated income, had expenses, or conducted any activity. If you don’t file, you could face fines and make it harder to dissolve the corporation in the future.

My company is incorporated in the UK but has a US client paying us royalties. Do we need to file Form 1120-F?

- Likely yes — especially if withholding tax was deducted from your royalty payments. You can disclose this income, apply any US-UK treaty reduction that applies, and get a refund for any taxes that were withheld too much by filing Form 1120-F. Even if you believe the treaty reduces your US tax to zero, filing a protective return is strongly recommended.

What is the difference between ECI and FDAP income for foreign corporations?

- Effectively Connected Income (ECI) is money you make by actively running a business or trade in the US. It is taxed at the usual progressive corporate rate, which is now 21%, after deducting permitted business expenses.

- Passive income like dividends, interest, rentals, and royalties make up FDAP (Fixed, Determinable, Periodical, or Annual income). A flat 30% withholding tax is usually taken out of gross income; however, a tax treaty may lessen it.

We missed the Form 1120 deadline. Can we still file? What are the consequences?

- Yes, it is advisable to file as soon as possible. The IRS can assess failure-to-file penalties (5% per month, up to 25%) plus interest on any unpaid tax. But it’s always better to file late than not at all. If you can show that you have a good reason for the delay ( such being sick, a natural calamity, or relying on a tax counsel), the fines may be lower in some situations.

Can a foreign firm that has a US LLC declare it doesn’t have to file Form 1120-F?

- This depends on how the US taxes the LLC. If the US LLC is recognized as a “disregarded entity” (a single-member LLC with no election), its actions go straight to the parent company in another country. For those activities, the foreign company may have to fill out Form 1120-F. If the LLC wants to be taxed like a corporation, it sends in its own Form 1120. It’s crucial to get this classification right, but it’s not always straightforward to do.

Is there a minimal income level that Form 1120 doesn’t apply to?

- No, C corporations don’t have to submit Form 1120 if they don’t make a specific amount of money.Even a corporation with $0 in revenue and $0 in tax liability must file if it is incorporated and exists as a legal entity. The only time a return is not required is after formal dissolution and IRS notification.

Could you please explain the branch profits tax on Form 1120-F and how it is calculated?

- Foreign companies with branches in the US have to pay an extra tax called the branch profits tax (BPT). It thinks of the branch as a US subsidiary that sends money to its parent company in another country. The BPT rate is usually 30%. It is based on the “dividend equivalent amount,” which is a way to figure out how much money you made after taxes that you put back into your business or gave away. Many US tax treaties lower this rate a lot. For example, the US-Netherlands treaty lowers it to 5%. Not including the BPT on 1120-F is a common and expensive mistake.

We are a business based in Germany. We haven’t done any business in the US or made any money from US sources since we got the EIN. Do we need to fill out Form 1120 or any other US tax return?

- You don’t need to fill out Form 1120 because it is just for businesses that are based in the United States. Even if a German business has an EIN, it doesn’t have to submit Form 1120.

- There is also no formal obligation to file Form 1120-F, provided the company genuinely had no US business activity and no US-source income. That said, we strongly recommend filing a protective return with zero income each year the EIN remains active. The fact that an EIN exists means the IRS has a record of your company: if the IRS were to later conclude that US activity did occur, the absence of a filed return would automatically deny you any deductions — tax would be assessed on gross income with no offsets. A protective filing eliminates that risk and requires minimal effort.